Global availability

Global payment management, we give merchants the ability to accept payments globally with stripe Build online revenue without payment management headaches, no matter where your clients are..

Minimize risk to maximize profit.

Early fraud warnings are notices generated to flag payments that are suspected to be fraudulent. An early fraud warning is created when a cardholder lodges a claim of fraud with their issuing bank and occurs before an official chargeback. as fraud disputes can incur a dispute fee.

Fraud detection is the process of identifying whether a transaction is fraudulent or not. This can be done through various means, such as analysing customer behavior or looking for patterns in the data that might indicate fraudulent cases.

Our payment services go above and beyond to protect you and your customers from fraudulent activity.

We provide security that saves you from worrying about fraud and theft so you can focus on your business.

Payske includes sophisticated fraud protection for merchants of every size, at no additional cost.

Payske is committed to protecting you, your business and your customers from fraudulent activities.

Rates by up to 99%

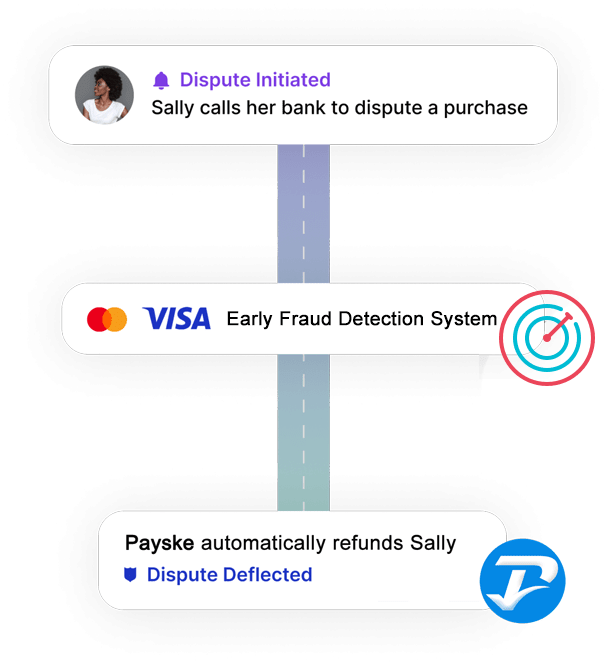

Early fraud warnings

is a dispute notification service that provides merchants with the opportunity to refund transactions prior to them turning into disputes. this will removes the concern of dealing with disputes so that you can focus on growing revenue and driving profitability.

Early fraud warnings

is a dispute notification service that provides merchants with the opportunity to refund transactions prior to them turning into disputes. this will removes the concern of dealing with disputes so that you can focus on growing revenue and driving profitability.

An early fraud warning is created when a cardholder lodges a claim of fraud with their issuing bank and occurs before an official dispute. An early fraud warning indicates that the card issuer has notified us that a charge may be fraudulent.

Each early fraud warning (was refunded) incurs a $5 fee, which is deducted from your payske balance. Only pay for the alerts you receive.

Early fraud warnings helps hypergrowth startups reduce chargeback rates by up to 99%

Early fraud warnings is the only solution on the market that covers Amex, Discover, Mastercard and Visa transactions, and others..

Features

Prevent chargebacks Protect your business.

Refund and intercept chargebacks before they become official disputes.

Foolproof way to kill disputes before you get dinged.

Avoid Payske account being suspended or terminated

Avoid getting put on high risk monitoring programs.

Obliterate your dispute rate

Accept more payments. with chargeback immunity, you can accept higher risk payments.

Thing to keep in mind: Automatically fully refunding an early fraud warning is the only way to prevent a dispute.

The Perils of a High Dispute Rate

Running an online business comes with its fair share of challenges, one of which is managing customer disputes. While disputes are an inevitable part of any merchant's journey, they can have serious ramifications if left unaddressed, particularly for sellers who rely on low-risk payment processors. In this article, we will explore the consequences of a high dispute rate and shed light on why merchants should strive to keep it in check.

Damage to Reputation

One of the most significant consequences of a high dispute rate is the potential damage to a merchant's reputation. Online shoppers heavily rely on reviews, ratings, and word-of-mouth recommendations before making a purchase. A high dispute rate signals to potential customers that there might be issues with the merchant's products or services, leading to a loss of trust. Negative reviews and poor customer feedback can harm brand reputation, resulting in decreased sales and customer acquisition.

Account Termination or Suspension

Low-risk payment processors typically impose certain thresholds and guidelines to ensure the smooth functioning of their platform. If a merchant's dispute rate exceeds these thresholds consistently, it may lead to account termination or suspension. Payment processors take disputes seriously as they can be indicative of fraud, poor customer service, or inadequate product quality. Losing access to a payment processor can severely impact a merchant's ability to process payments, disrupting their business operations and potentially leading to financial loss.

Increased Processing Fees

Merchants with high dispute rates often face financial penalties imposed by payment processors. These penalties are typically in the form of chargeback fees, where the merchant is required to cover the cost of the disputed transaction, as well as additional fees levied by the processor. Moreover, payment processors may also increase processing fees for merchants with a history of high dispute rates. These added expenses can eat into profit margins and make it challenging for merchants to maintain a viable business model.

Difficulty in Obtaining New Payment Processing Solutions:

Once a merchant's account has been terminated or suspended by a low-risk payment processor due to a high dispute rate, finding an alternative payment processing solution becomes significantly more challenging. Other processors may view a history of high disputes as a red flag, making it harder for the merchant to secure a new payment processing account. This can lead to extended periods without payment processing capabilities, resulting in lost sales and a potential setback for the business.

Legal Consequences and Compliance Issues

In some cases, a high dispute rate may trigger legal consequences and compliance issues for merchants. Excessive chargebacks can attract the attention of regulatory bodies and law enforcement agencies, who may investigate the merchant for potential fraud or deceptive practices. Non-compliance with payment processor guidelines, such as failing to respond to disputes within specified timeframes, can result in further legal complications, fines, and reputational damage.

Conclusion

Merchants relying on low-risk payment processors must be diligent in managing their dispute rates to avoid the dire consequences that can arise from a high dispute rate. From reputation damage and account termination to financial penalties and legal consequences, the implications can be significant and long-lasting. By prioritizing excellent customer service, maintaining transparent business practices, and promptly addressing customer concerns, merchants can mitigate disputes and foster a positive customer experience. Remember, a low dispute rate is not only crucial for maintaining a healthy merchant-processor relationship but also for sustaining a thriving online business.

Fraud protection.

We offer a three-tier defense strategy to identify fraudulent activity and keep fraud from impacting your operations.

The goal is to call out the fraudulent activity before it happens,

Fraud detection techniques and algorithms.

A range of data analytics techniques and algorithms are employed to detect and mitigate fraud risks effectively.

Radar for Fraud Prevention

Radar for Fraud Prevention

is a suite of modern tools to help you fight fraud. It’s fully integrated into your payments flow and you can start using it without any additional development time or cost.

3-D Secure

3-D Secure is a technology that helps verify a cardholder's identity with an additional layer of security. Along with the card number and CVV, an authentication code (sometimes referred to as OTP) is usually required by the cardholder's issuing bank. In theory, only cardholders will know the password; fraudsters shouldn’t know it and, therefore, won’t be able to complete the transaction.

3D Secure Version 2

3D Secure 2 : An authentication standard that reduces fraud and provides additional security

The 3D Secure standard—often known by its branded names like Visa Secure, Mastercard Identity Check, or American Express SafeKey—aims to reduce fraud and provide added security to online payments.

3D Secure 2 (3DS2) introduces “frictionless authentication” and improves the purchase experience compared to 3D Secure 1. It is the main card authentication method used to meet Strong Customer Authentication (SCA) requirements in Europe and a key mechanism for businesses to request exemptions to SCA.

Payske supports 3D Secure 2.Your integration runs 3D Secure 2 when supported by the customer’s bank and falls back to 3D Secure 1 otherwise.

Payment Fraud Management to Scale Globally, Risk-Free

Payment Fraud Management to Scale Globally, Risk-Free

Payment Fraud Management and International Compliance is Not Something

Your Team Needs to Worry About

When selling internationally, payment fraud management and compliance with international regulations are big issues. The good news is that

we take care of both, so you can concentrate on growing your business.

We Protect You Against Payment Fraud

Your security is paramount in everything we do. Our services go above and beyond to protect you and your customers from

fraudulent activity. We provide security that saves you from worrying about payment fraud and theft.

Upgraded Fraud Detection Tools

Upgraded Fraud Detection Tools

We offer a multi-tier defense strategy to identify fraudulent activity and keep it from impacting your operations. Our algorithms are proprietary to our business and customized to different industries and geographies. We use a combination of artificial intelligence and manual review processes to make sure our fraud-detection mechanisms are optimized, keeping fraud to a minimum.

Crushing False Positives

These same anti-fraud mechanisms also ensure as little interference as possible with good orders, as unnecessary fraud alerts can negatively affect your authorization and conversion rates, bottom line, and customer satisfaction.

What is payment fraud?

Payment fraud is a type of financial fraud that occurs when someone intentionally uses false or stolen payment information to make a purchase. For example, fraudulent actors might use stolen credit card information, create fake checks, or make unauthorized electronic fund transfers.

Retail businesses are particularly vulnerable to payment fraud, since they deal with a large volume of transactions and may not have the resources to thoroughly vet each payment method. Payment fraud can result in significant financial losses for businesses, damage to their reputation, and legal liabilities.

Credit Card Fraud.

Data analytics plays a pivotal role in the detection and prevention of credit card fraud. It involves the analysis of transaction data, patterns, and user behavior using machine learning algorithms.

For example, if a credit card is suddenly used for transactions in various geographic locations in a short period, the system can trigger an alert. Data analytics can also establish benchmarks for typical spending habits, making it easier to identify deviations. Real-time monitoring can proactively block suspicious transactions.

There are several types of payment fraud

Credit card fraud: is the unauthorized use of a credit card to make purchases or obtain cash. For instance, this fraud can involve the use of stolen credit card information or the creation of counterfeit credit cards. In credit card fraud, the fraudster can use the stolen credit card to make purchases online or in-person, or they may use the card to withdraw cash from an ATM.

Debit card fraud: is similar to credit card fraud but involves the unauthorized use of a debit card. The fraudulent actor may use a stolen debit card or the card information to make purchases or withdraw cash from an ATM. Debit card fraud can also occur if someone obtains access to the PIN associated with the card.

Bank fraud: refers to any type of fraud that involves a bank or financial institution. This can include fraudulent loans, account takeover fraud, and identity theft. Bank fraud can result in significant financial losses for individuals and institutions.

Wire transfer fraud: occurs when a fraudulent actor obtains access to someone’s bank account or wire transfer information and then uses it to transfer money to their own account. The fraudulent actor may employ various tactics to obtain the victim’s information, including phishing scams or hacking into the victim’s computer or email account.

Check fraud: involves the creation or alteration of a check to obtain funds fraudulently. This can include forging a signature or altering the amount of the check. Check fraud can occur when someone steals a checkbook or obtains access to a victim’s checking account information.

Mobile payment fraud: is the unauthorized use of mobile payment services, such as Apple Pay or Google Wallet, to make purchases or transfer funds. This can occur if someone gains access to the victim’s mobile device or payment information. Mobile payment fraud can also occur if a fraudulent actor creates a fake mobile payment account using someone else’s information.

Scale your business globally with Payske platform.